SINGAPORE PROPERTY

Have you ever thought that the local property market scene is too boring and sluggish and consider to look beyond Malaysia to purchase an overseas property or have some diversification your property portfolio or a hedge against Malaysian Ringgit against other foreign currencies, or to get an accommodation for those who send their children for oversea education.

We at PROPCAFE are pretty sure that many of us may have this idea in mind and it also comes with a bragging right.

Picture this:

Our parents will probably be quite enthusiastic than us about the fact that we have an oversea property and can’t wait to have vacation abroad and share this in makan-makan gathering with family, FB stories, Ista stories, free marketing promo, happy kan?

If you have made up your mind that you need to venture into oversea property investment. Look no further, we have some recommendation for you. Let us narrow now the country you should park your money in.

A place that is just 1km from Malaysia. That is Singapore.

Why Singapore Property

Buying property is an long term investment, while looking at Singapore, we would say we are quietly optimistic about Singapore and here are the reasons.

Political Stability

We know how important is that given what has happened recently in Sheraton Hotel in PJ. There is also a Sheraton in Singapore too if you are curious and they are located in Newton.

Source: https://www.oyster.com/singapore/hotels/sheraton-towers-singapore/

Pro Business Environment in Singapore

It is easy to set up businesses in Singapore, you can do it online. It is even easier to transact with government, almost all transaction can be done online, no surprise here, that even in the midst of COVID-19 recession more companies are setting up in Singapore.

https://www.straitstimes.com/business/more-new-business-entities-set-up-in-singapore-despite-covid-19-recession

Low and Transparent Tax Regime

Headline corporate tax is at 17%, while GST is 7%, personal income tax ranges from 2 to 22% while property tax is taxed based on annual value depending on own occupation or lease out, you can read it all here.

Safe Haven Status

This is debatable while we would say the strength lies on the SGD denominated notes. The Monetary Authority of Singapore (BNM equivalent) takes an approach that appeals to investors in our view at lease, MAS monetary policy framework is centred on managing the Singapore dollar against a trade-weighted basket of currencies. This is also known as the Singapore dollar nominal effective exchange rate (S$NEER). We also observe that it is comparatively much easier to remit money out of Singapore eventually upon divestment against its ASEAN peers.

Low Interest Rate Regime

Housing loan rate ranging from 1.5% to 2% as at the time of this write up, it means that you can gear up more, since interest rate is considered low.

Government’s Proactive Role in Stabilizing the Property Market Price

Stringent property cooling measures are in place to reduce speculations. The pro is the properties price remain relatively stable, less speculative. The land sales are controlled by the government, hence supplies are controlled. The con is there are a lot of restrictions in place. Most people in Singapore don’t own multiple residential properties.

So we have talked about the goods what about the negatives of property investment in Singapore.

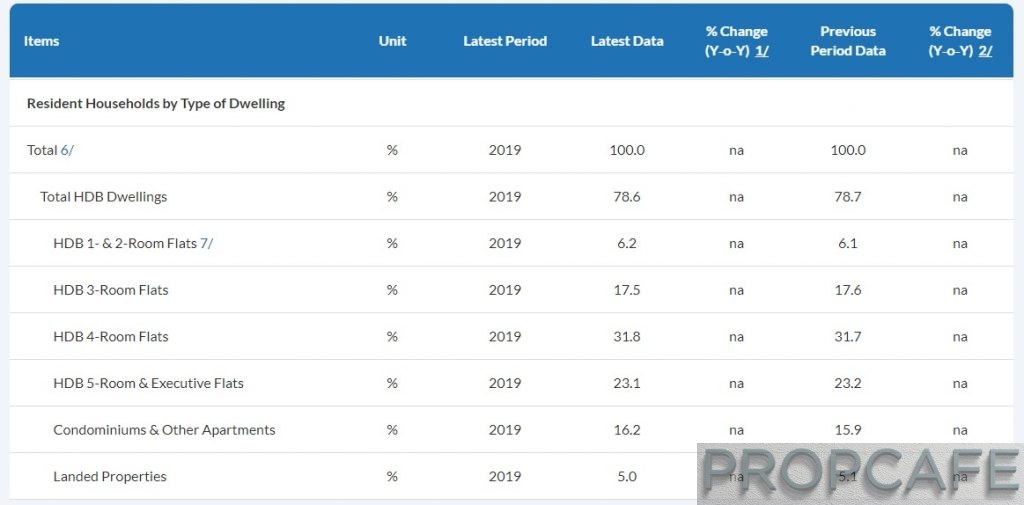

There Are More Condos Than Landed Properties

Singapore is a city, land of scarcity, an inch of land is an inch of gold. 95% of residential housing type are either HDB flats of condo, meanwhile 5% are residential landed properties.

Almost 80% of the Singapore populations live in HDB, public housing flat, while 20% live in condo and landed properties.

Landed properties in Singapore do attached with high price-tag with average price at >$1.6m.

So basically, just trying to say if one is with limited budget you can probably look at smaller size condos. If got budget, itu kan lain cerita.

High Entry Barrier

MYR against SGD. RM3 is SGD1, you do the maths.

1 bedroom condo will cost about $700,000 SGD or RM2.1 million. You can’t purchase the public housing or the HDB flat if you are not Singaporean or Permanent Resident. You may get some information here on the eligibility to purchase a HDB flat.

High Cash Call Up Front

Maximum margin of financing being 75% of SPA Price

Stamp Duty: 3% of SPA Price

Additional Buyer’s Stamp Duty (ABSD) 20% on top of the SPA price if you are buying as a foreigner.

Let’s work out some numbers and get ready a budget and some cash for some serious property shopping in Singapore.

Say the budget you are looking at is $700,000.

The estimated up front cost will be:

|

25% down payment |

$175,000 |

RM525,000 |

5%, 20% 3 mths from OTP |

|

3% stamp duty |

$15,600 |

RM46,800 |

2 weeks from OTP |

|

20% ABSD |

$140,000 |

RM420,000 |

2 weeks from OTP |

|

Legal Fees |

$3,000 |

RM9,000 |

|

|

Total |

$333,600 |

RM1,000,800 |

|

You need approximately RM1mil ready before shopping around for properties in Singapore. In terms of % for cash out lay, we are looking at approximately 50% down payment if you are purchasing it as a foreigner, it is pretty steep right barrier entry.

So you are still interested in investing in Singapore?

If you do, hang in there. Get your coffee ready and we will share with you how it is done!